An Industry at a Crossroads

The insurance sector stands at a pivotal crossroads between its legacy roots and a digital future. Cloud migration has emerged as a powerful catalyst for this transformation, promising new levels of agility, cost efficiency, and innovation. By shifting core systems onto modern cloud platforms, insurers aim to meet rising customer demands for speed, personalization, and transparency – all while contending with strict regulations and fierce competition. Cloud adoption is now mainstream: over three-quarters of insurance companies have moved at least some operations to the cloud, and one recent survey found 91% of banks and insurers have initiated their cloud journey. Cloud is no longer viewed as a mere IT upgrade, but as a strategic lever for greater efficiency, resilience, and speed to market in an industry historically encumbered by legacy technology.

Yet this transition is not without challenges. Modernizing decades-old, mission-critical systems involves significant risk and complexity. Large insurers still run most core functions on aging mainframes and COBOL-based platforms, and the push to modernize them comes with a complex risk calculus. For example, only about 10% of large insurers have modernized more than half of their core systems– meaning the vast majority of critical applications still run on legacy infrastructure. On average, insurers spend 70% of their IT budgets just to maintain these legacy systems, draining resources that could otherwise fund innovation. The case for modernization is compelling (outdated systems hinder agility, inflate costs, and pose talent and security challenges), but the execution risks are equally real. In fact, McKinsey analysts predict over $100 billion in cloud migration spend may be wasted in coming years due to missteps, with 75% of projects running over budget and 38% behind schedule. In a sector that handles sensitive customer data and high-stakes transactions, a failed or poorly executed migration isn’t just an IT problem – it can disrupt business operations and even threaten regulatory compliance.

To balance urgency with caution, many insurers are eschewing “big bang” cutovers in favor of phased, incremental cloud migration. Rather than attempting to replace every system at once, a phased approach modernizes one subsystem or business capability at a time, reducing the likelihood of major downtime or customer impact. Each step can be tested and validated in isolation, ensuring legacy and new cloud systems co-exist smoothly during the transition. For instance, an insurer might first migrate non-critical workloads or customer-facing portals to the cloud, gain experience, and then gradually tackle core policy or claims systems. By leveraging techniques like real-time data replication to keep legacy databases in sync with cloud databases, firms can achieve transformation goals without a risky “all-at-once” overhaul. In short, success lies in a carefully managed journey: modernize what’s necessary, mitigate risks at each phase, and never lose sight of core business continuity.

Importantly, a new enabler has emerged to support this phased cloud journey: Infrastructure as Code (IaC).

As discussed below, IaC is becoming a strategic linchpin in insurance IT modernization. By managing infrastructure through code, insurers can standardize and automate each step of cloud onboarding, greatly reducing human error and configuration drift between legacy and cloud environments. This approach allows cloud migrations to proceed in controlled, repeatable phases, with the confidence that each environment (dev, test, prod – on-premises or cloud) is configured exactly as intended. In the following sections, we explore how IaC is woven into the fabric of modern insurance cloud strategies – enabling consistent hybrid deployments, improving security, and aligning with DevSecOps best practices – alongside the broader challenges of cloud migration in insurance.

Modernizing Legacy Systems: Imperative vs. Risk

Decades of accumulated legacy technology have left insurers with a pressing modernization imperative – and a delicate risk balance. As noted, only a small minority of insurers have significantly modernized their core platforms, while most still rely on systems designed in the 1980s or 90s. These aging systems are costly to maintain (often 70%+ of IT spend) and slow to adapt, hindering an insurer’s ability to launch new products or digital services. Moreover, the workforce with skills to maintain older mainframes is shrinking due to retirements. The need to modernize is crystal clear: outdated core systems hamper agility, inflate operating costs, and introduce operational risks (from outages to security vulnerabilities).

However, modernizing core insurance systems carries significant execution risk. The process is often compared to rebuilding the airplane while flying it – any disruption can directly impact customers and financial results. We’ve seen how frequently large-scale transformations falter without careful planning. McKinsey estimates that through 2024, enterprises will waste over $100B on cloud migration efforts that don’t meet their goals, with the majority of projects exceeding budgets or timelines. The insurance industry’s own history includes cautionary tales of core system replacements that ran aground, causing customer service failures or regulatory issues. In this context, leaders must approach core modernization with meticulous risk management: strong governance, staged milestones, and contingency plans for when surprises inevitably arise.

A phased modernization strategy is therefore the preferred route for many insurers. Instead of a risky “big bang” where a legacy policy admin system is turned off one day and a new cloud system is turned on the next, most firms opt for incremental steps. For example, an insurer might first modernize peripheral modules (like document management or rating engines) and interface them with the legacy core via APIs. Gradually, new cloud-based components take over more functions until the legacy core can be decommissioned. Each phase is run in parallel with the old system for a time, to validate outputs and ensure nothing critical is missed. This approach trades immediate gratification for risk reduction – a prudent trade-off in a risk-averse industry.

Infrastructure as Code plays a strategic role in enabling this phased approach. By defining infrastructure and environments through code, IaC allows IT teams to spin up test environments that mirror production, rehearse migrations safely, and automate rollbacks if needed. For instance, before migrating a core underwriting system, an insurer can use IaC tools (like Terraform or CloudFormation) to provision a full sandbox environment in the cloud that replicates the on-premises setup – networks, servers, middleware, configuration – all defined in code.

This environment can be repeatedly deployed for testing the migration process until it’s perfected. Because the configurations are codified, there’s no chance of a forgotten setting or misconfigured server derailing the cutover. IaC essentially serves as a safety net, ensuring each incremental migration is done in a controlled, repeatable manner.

It also makes it easier to run systems in parallel during transition: any change to the legacy environment (say a new product or rate change) can be applied via code to the cloud environment as well, eliminating configuration drift between old and new. This dramatically lowers the risk that something works in testing but fails in production. In short, IaC gives insurers a powerful toolkit to modernize legacy systems with high confidence – enabling predictable deployments, fast rollback if needed, and consistent setups across every stage of the migration.

To illustrate, consider a simple example of Infrastructure as Code in action. Using a tool like Terraform (an open-source IaC framework), an operations team can define an entire network and server infrastructure in a configuration file, instead of clicking through cloud consoles or manually configuring settings. For example, the code below provisions an Azure resource group and virtual network for a new insurance application environment:

# Terraform script to define Azure infrastructure

resource "azurerm_resource_group" "core_insurance_rg" {

name = "CoreInsurance-RG"

location = "East US"

}

resource "azurerm_virtual_network" "core_insurance_vnet" {

name = "CoreInsurance-VNet"

address_space = ["10.10.0.0/16"]

location = azurerm_resource_group.core_insurance_rg.location

resource_group_name = azurerm_resource_group.core_insurance_rg.name

}

With these few lines of code, the necessary cloud resources are described declaratively. Deploying them is as simple as running the CLI command terraform apply. The IaC tool reads the configuration and automatically creates or updates the cloud infrastructure to match the desired state. This exact process can be repeated in a test environment, in a production environment, or even in a disaster recovery region – ensuring each is identical. If a change is needed (say, adding a subnet or tweaking a security group), the team updates the code and re-applies it, rather than manually adjusting each environment. The benefits during a phased migration are enormous: every environment stays in sync, there’s an automatic audit trail of changes (because the code can be stored in Git), and manual errors are virtually eliminated. Leading insurers have recognized that adopting IaC is essentially insurance for their cloud migration – it codifies best practices and guards against the very errors that often derail complex projects.

Infrastructure as Code: A Strategic Enabler in Phased Cloud Migration

Moving to the cloud is as much about how you migrate as what you migrate. This is where Infrastructure as Code (IaC) has become a game-changer for the insurance industry. IaC refers to managing and provisioning infrastructure (servers, networks, configurations, and more) through machine-readable definition files rather than manual setup. In practice, your infrastructure is treated as software – stored in code repositories, versioned, tested, and executed on demand. This approach brings a new level of rigor and agility to cloud onboarding, especially for complex, phased migrations.

Strategically, IaC enables insurers to migrate in phases with confidence and control. In a phased migration, multiple environments (legacy on-prem, new cloud, and often intermediate hybrid stages) must run concurrently without falling out of sync. Traditionally, keeping configurations consistent across these environments is difficult – a tweak in a firewall rule on-prem might not be replicated in the cloud environment, leading to inconsistencies or security gaps (the dreaded “configuration drift”). IaC solves this by ensuring that every environment is defined from the same source of truth.

As IBM describes, IaC eliminates the human errors and drift that lead to vulnerabilities, enforcing consistent configurations across dev, test, and production. For example, if an insurer needs to deploy an update to a core claims system in both its private cloud and a public cloud test sandbox, an IaC script can apply the identical configuration to both. This consistency dramatically reduces the risk of surprises when cutting over from old to new systems.

Moreover, IaC brings speed and repeatability to what used to be slow, one-off operations. Automations replace manual setup, so environments that once took weeks to configure can be spun up in hours or less. One industry analysis noted that with IaC, companies get “faster deployments, fewer errors overall, consistent environments, and the ability to quickly and easily scale infrastructure — without sacrificing control.”

For insurers, this means new cloud environments for testing or new product launches can be created on-demand, following the exact specifications required by security and compliance. Teams can teardown and rebuild environments at will, knowing they will come up the same way every time. This repeatability not only accelerates project timelines but also acts as a safety net – if a deployment fails or a configuration doesn’t work as expected, the team can quickly revert to a previous stable state by re-applying the last known good code (since every change is tracked in version control).

Equally important, IaC embeds governance and best practices into the migration process. Because infrastructure changes go through code, they can leverage the same version control and peer review processes as application software. Every infrastructure change can be tied to a code commit, triggering automated checks: syntax validation, security scanning (using tools like Checkov or Sentinel), and integration tests in a CI/CD pipeline.

This aligns perfectly with DevSecOps principles, where security and compliance are built into the development lifecycle rather than bolted on later. In effect, IaC provides an audit trail by default – you can see exactly who changed what, when, and why, simply by looking at the Git history of your infrastructure repository. This level of transparency is a boon in a regulated industry. As one tech writer put it, “When infrastructure becomes code, it becomes visible – version control creates audit trails and rollback options, and consistent environments reduce the risk of issues in testing or compliance reviews.”

Auditors and risk officers appreciate that changes to a claims database server’s configuration, for example, aren’t happening ad hoc on a console – they’re proposed in code, reviewed, approved, and logged.

During an insurance cloud migration, IaC therefore acts as a bridge between IT execution and governance. Cloud and DevOps leaders should prioritize IaC adoption early in the modernization journey.

Doing so establishes guardrails that keep the migration on track. It means from day one, environments are defined in a structured manner, reducing the chaos that often accompanies complex projects. For instance, when migrating an underwriting system, IaC can enforce that all cloud instances use approved machine images, with the correct patch levels and security agents installed – automatically, through code.

Configuration policies (like encryption standards or network segmentation rules) can be codified so that any environment deployed meets corporate security requirements by design. This policy-as-code approach ensures that compliance isn’t an afterthought; it’s baked into how infrastructure is provisioned. In practical terms, insurers using IaC have found that they can achieve DevSecOps alignment more readily: infrastructure changes undergo the same scrutiny as code changes, and security teams can insert automated controls (for example, disallowing any open ports except 443, or requiring encryption on S3 buckets) that will stop non-compliant infrastructure changes from being applied.

From an executive perspective, treating IaC as a strategic priority yields long-term dividends. It not only lowers risk during the cloud migration program, but also sets the company up for operational excellence post-migration. After all, moving to the cloud is not a one-time event – it’s a new operating model.

IaC helps ensure that once you’re in the cloud, you don’t recreate the same silos and drift that plagued your on-premise world. Everything remains documented in code, making maintenance and future changes far easier and less error-prone. Teams spend less time firefighting misconfigurations and more time delivering value. In fact, enterprise surveys show that automation technologies like IaC significantly boost IT team productivity.

For insurance CIOs seeking to do more with constrained resources, that productivity gain is critical. It means your talent can focus on building new capabilities (like that AI-driven risk model or customer mobile app) rather than manually tweaking servers and networks.

In summary, Infrastructure as Code has moved from a DevOps experiment to an enterprise imperative in the insurance industry. It underpins the ability to execute phased migrations smoothly, maintain consistency across hybrid environments, and achieve the holy grail of “faster, better, cheaper” all at once. As the following sections will further illustrate, IaC also dovetails with other key cloud migration considerations – from managing hybrid architectures to controlling costs – making it an essential pillar of any modernization roadmap.

Cloud Cost Realities

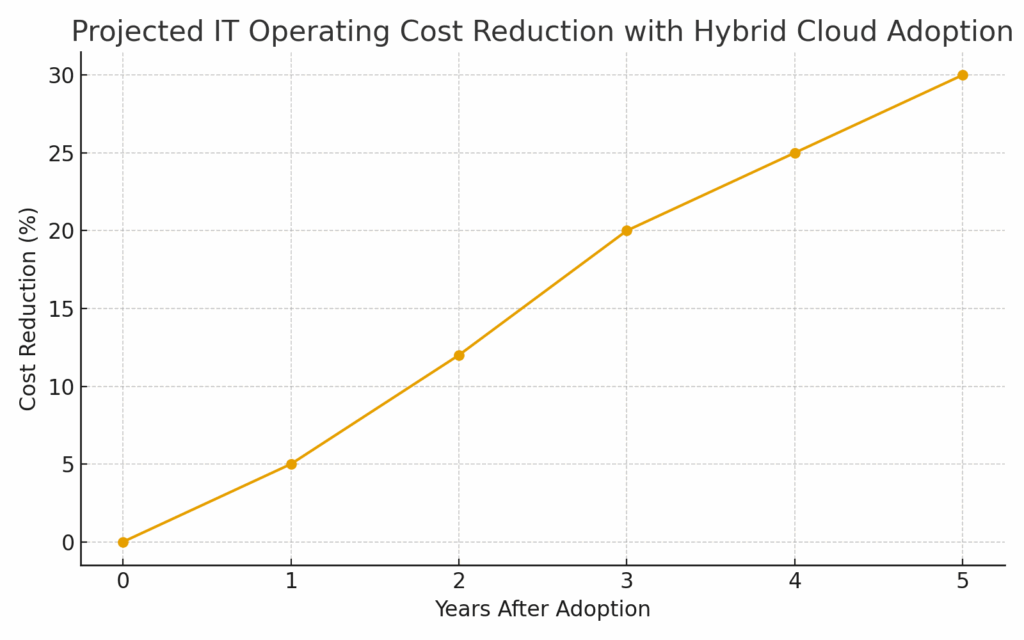

CFOs and CIOs in insurance often look to cloud migration as a way to rein in IT costs – and indeed the potential savings can be significant. By retiring on-premise data centers and leveraging cloud’s pay-as-you-go model, insurers can avoid heavy capital expenditures and only pay for the compute/storage they actually use. Studies have found that successful cloud migrations deliver on average 20–30% infrastructure cost savings due to more efficient resource utilization and elimination of excess capacity. In one analysis, McKinsey estimated cloud adoption could reduce IT infrastructure spending by about 30% for typical companies, thanks to on-demand scaling and offloading maintenance to cloud providers.

Many insurers cite cost optimization as a key driver for cloud adoption. And when executed well, the results are encouraging: over half of IT leaders report measurable cost reductions after migrating systems to the cloud, with overall IT expenses reduced by roughly 15–20% on average. These gains come from rightsizing infrastructure, turning off idle resources, leveraging cheaper cloud storage tiers, and reducing the personnel effort required for upkeep of physical hardware.

However, the cloud’s cost benefits are not automatic – and the reality can sometimes defy expectations. Without disciplined cost management (“FinOps”), cloud expenses can escalate rapidly and unexpectedly. A cautionary example comes from GEICO, a major U.S. insurer, which saw its public cloud bill balloon to over $300 million per year after an aggressive push of workloads to a hyperscale cloud. The company found that certain steady-state, high-volume workloads were actually more expensive in public cloud than on efficient in-house infrastructure. In response, GEICO decided to repatriate a large portion of its workloads back to a private cloud and optimized data centers – and in doing so, slashed compute costs by 50% per core and storage costs by 60% per gigabyte compared to the public cloud. This dramatic outcome underscores a broader point: for some use cases, cloud can indeed be more costly if not managed carefully. Insurance workloads that run 24/7 at high utilization (e.g. core mainframe transactions) may not gain much from cloud’s elasticity and could incur premium pricing for equivalent capacity.

GEICO’s experience is a high-profile example of what industry observers call “cloud repatriation” – pulling specific workloads back on-premises when economics or control considerations change. More broadly, surveys find many enterprises are recalibrating their cloud strategies to optimize cost. For instance, one study noted that up to 30% of cloud spend is often wasted due to inefficient use or lack of oversight. Without clear visibility, teams might over-provision resources, leave VMs running unused, or use expensive services that aren’t needed. In insurance, where margins are thin and every expense draws scrutiny, a surprise cloud bill can quickly erode the expected benefits of migration.

The takeaway for insurers is that cloud economics require active governance. Achieving cost savings isn’t as simple as “lift and shift everything and voilà, costs go down.” Those who realize the efficiency upside typically invest in FinOps practices – i.e., financial discipline applied to cloud. This includes continually monitoring usage, rightsizing instances, setting up budget alerts, and negotiating committed-use discounts with providers. It’s also about architectural choices: using spot instances for non-critical jobs, leveraging cloud-native services that auto-scale down, and avoiding redundant data egress costs by thoughtful placement of workloads. In many cases, a hybrid architecture (discussed next) plays a role in cost optimization, allowing companies to keep certain workloads on private infrastructure where they run most cost-effectively, while using public cloud for the elastic or spiky workloads (like usage-based customer portals or AI model training) that benefit from on-demand scaling.

Infrastructure as Code contributes to cost control as well. By codifying infrastructure deployments, IaC makes it easier to implement automated policies that curb waste. For example, engineers can write IaC scripts to schedule the shutdown of non-production environments after business hours, or to enforce that every development VM is tagged with an owner and expiration date. These policies, executed as code, prevent “zombie” resources from running indefinitely and racking up charges.

IaC also facilitates cost reviews as part of the deployment pipeline – e.g., a pull request to instantiate a new database can be programmatically checked against cost thresholds or require approval if it exceeds a certain size. In short, infrastructure defined in code is inherently more observable and governable. Leading insurers are starting to integrate cost metrics into their IaC pipelines (sometimes called “InfraSecOps” or FinOps automation), ensuring that cloud cost management is a continuous process, not a quarterly surprise.

Ultimately, cloud can absolutely deliver cost savings and enhanced ROI for insurers – but it won’t happen by itself. It requires a combination of smart architecture, ongoing optimization, and governance tooling. The cloud’s variable cost model is a double-edged sword: it can eliminate waste, but can also introduce volatility. By using IaC and related practices, insurers turn cloud spending into something they can monitor and adjust in near-real-time. With careful planning and the right controls in place, insurers can realize the cloud’s efficiency promise while avoiding the budget traps. Cloud migration, done right, becomes not just an IT upgrade but a financially prudent strategy for the long run.

Integration Complexity in a Legacy Landscape

For many insurers, the technical heart of cloud migration challenges lies in integration – specifically, connecting modern cloud applications with decades-old legacy systems. Industry executives routinely cite legacy integration as their number-one hurdle in cloud projects. It’s easy to see why: insurance IT estates often include mainframe-based policy administration, claims, billing, and underwriting systems that were never designed for open connectivity.

These older systems may use proprietary data models, outdated protocols, or even flat-file exchanges that make real-time integration difficult. As a result, migrating an insurance workflow to the cloud isn’t as simple as turning on a SaaS application – you must also bridge that application back into the old world. If a new cloud-based claims portal can’t fetch policy data from the mainframe policy admin system, it’s not very useful.

Integration complexity manifests in several ways. Data formats might be incompatible (e.g. one system uses EBCDIC encoding or ancient COBOL copybooks, while new cloud apps expect JSON/XML). Documentation for legacy APIs (if they exist) is often sparse, and the experts who understand them might have retired. Each workaround or custom adapter adds potential fragility. It’s not uncommon for insurers to find that the “last 20%” of a cloud project – wiring it into all the necessary back-end systems – takes as much effort as the first 80%. In short, cloud migration in insurance is not a greenfield exercise; it’s a brownfield integration project in many respects.

How are forward-looking insurers tackling this integration puzzle? A few strategies are emerging. One is the use of API layers and middleware to abstract legacy systems. Rather than connecting a cloud app directly to a 30-year-old mainframe, the insurer might implement an API gateway or integration platform (possibly in the cloud or on-prem) that interfaces with the mainframe using whatever means available (MQ messages, stored procedures, etc.), and exposes modern RESTful APIs to the new cloud services. This essentially wraps the legacy system with a modern facade, translating between old and new. We see insurers investing in integration-platform-as-a-service (iPaaS) solutions, or building microservices that act as brokers between cloud and core. Another tactic is real-time data replication and streaming.

For example, using tools to replicate mainframe DB2 or VSAM data to a cloud database in near real-time, so that cloud applications can read (or even write) to a synchronized dataset without hammering the legacy system directly.

It must be acknowledged that solving integration is as much about people and process as technology. Many insurers are upskilling their teams in modern integration techniques (like event-driven architecture, use of JSON/REST, etc.), and instituting agile practices so that business and IT stakeholders iterate on integration requirements. They treat integration work as a first-class deliverable in any migration project, not an afterthought. Governance is key too – mapping data flows, securing data in transit, and ensuring compliance (e.g. PII data moving to cloud must be encrypted and audited).

While Infrastructure as Code doesn’t eliminate the inherent complexity of making old and new systems talk, it can assist in managing the integration infrastructure needed. For instance, an insurer might use IaC to deploy an integration tier (like an API gateway cluster or an ESB in the cloud) in a consistent, reproducible way. If each environment (dev, QA, prod) gets the same configured integration middleware via code, there’s less chance of an environment-specific bug derailing testing. IaC can also codify network configurations (VPNs, VPC peering, etc.) that connect cloud resources back to on-prem data centers, ensuring that these critical linkages are properly set up and not left to error-prone manual processes. In other words, IaC handles the “plumbing” pieces of integration reliably: the connection endpoints, security groups, subnets, and load balancers that your integration components rely on will be there as expected. This allows integration specialists to focus on the data and application logic, rather than worrying if a firewall port was missed in one environment.

Ultimately, conquering integration complexity is essential to unlock the full value of cloud migration. A cloud-based rating engine or AI analytics platform won’t shine if it operates in isolation from policy and claims data. Insurers that navigate this challenge well treat integration as a core competency. By combining modern tools (APIs, event streaming) with disciplined practices (like IaC automation and continuous integration testing of interfaces), they can ensure that their new cloud innovations seamlessly extend – rather than break – the value of legacy investments. The result is an IT landscape where old and new coexist productively: policy transactions from a COBOL system flow into a cloud data lake in real time; underwriting decisions made by a cloud AI service are fed back into an on-prem policy admin record; customers get a unified experience even though behind the scenes multiple generations of technology are working in concert.

The Hybrid Architecture Imperative

Given the mix of old and new technologies in insurance, hybrid cloud architectures have become the de facto strategy for most insurers. Rather than an all-or-nothing move to public cloud, insurers are blending on-premises and cloud environments to get the best of both worlds. In fact, industry analysis shows that roughly 73% of insurance companies favor a hybrid cloud model as their primary approach, compared to only 9% relying exclusively on public cloud. This high adoption of hybrid strategies underscores an important reality: for large insurers with critical legacy platforms, a hybrid architecture isn’t a temporary workaround – it’s a necessary and often long-term operating model.

Hybrid cloud (green) clearly dominates in the insurance industry at 73% adoption, compared to only 9% of insurers using public cloud alone (orange). This reflects the sector’s preference for a balanced cloud/on-premises strategy, allowing gradual modernization while keeping sensitive systems in controlled environments.

The appeal of hybrid cloud is its flexibility and risk mitigation. Immovable, sensitive systems can remain on-premises or in private clouds (where an insurer has dedicated infrastructure and full control), while new workloads and customer-facing applications migrate to public cloud services.

This allows an insurer to modernize incrementally, without risking core data or abruptly disrupting services that are better kept in a controlled environment. For example, an insurer might keep its core policy administration system on a private mainframe cloud due to stability and latency concerns, but run new mobile apps, portals, and AI analytics in the public cloud.

The two environments are tightly integrated (via secure network links and APIs), creating a single logical platform from a business standpoint. The hybrid approach also aligns well with regulatory and data sovereignty requirements, which often mandate certain data to stay within specific jurisdictions or on certified infrastructure. An insurer operating in countries with strict data privacy laws might keep customer PII and financial data on-prem or in a local private cloud, even as it uses global public cloud services for less sensitive workloads. As one report noted, hybrid cloud offers insurers an optimal blend of flexibility, control, security, and compliance alignment, ensuring each type of data and workload resides in the “right” environment. At the same time, hybrid setups deliver much of the cloud’s upside – scalability on demand, access to advanced cloud services (AI, IoT, etc.), and improved data availability across the enterprise.

Crucially, hybrid architecture is also an enabler of innovation. Insurers can rapidly deploy new digital capabilities in the cloud (from AI-driven analytics to omnichannel customer apps) and connect them back to on-prem core systems in real time. This “best-of-both-worlds” approach means an organization isn’t held back by its legacy estate, but also isn’t forced into a risky mass migration before the business is ready.

Over time, as confidence and cloud-native skillsets grow, more of the workload can shift cloud-ward – but even then, many insurers expect to retain a hybrid model for the foreseeable future. It provides a valuable safety net and a bridge between the past and future of insurance IT. In short, embracing hybrid cloud is about meeting the industry where it is: leveraging cloud innovation where it makes sense, while responsibly managing the systems that still run the business.

Managing a hybrid cloud at enterprise scale, however, introduces operational complexity of its own. There’s truth in the adage that hybrid can be “the worst of both worlds” if not done right – you have to maintain legacy systems and new cloud tech simultaneously. Here again, Infrastructure as Code has become indispensable. IaC gives insurers a fighting chance at taming hybrid complexity by using one set of tools and definitions across all environments. Teams can employ a cloud-agnostic IaC tool like Terraform or Pulumi to define infrastructure that spans both on-prem and cloud. For example, you could codify the setup of an on-prem VM cluster for a core insurance system and the provisioning of an AWS VPC for a connected cloud app in the same Terraform configuration.

This ensures that infrastructure in both worlds is deployed following the same playbook, with no drift. As a result, operations teams aren’t juggling completely separate processes or configurations for on-prem vs. cloud – they orchestrate both through code. An IBM expert noted that manual processes that once managed a few on-prem servers cannot handle today’s multi-cloud sprawl; IaC is essential for operating at scale across thousands of resources and multiple environments.

Concretely, consider an insurer running a hybrid data pipeline: on-premises mainframe data is ingested, then processed in a cloud analytics service. Using IaC, the networking (VPNs, subnets) connecting the two, the middleware that bridges them (message queues, data stream services), and the analytics clusters can all be deployed and configured consistently with one execution. If something in the pipeline needs to change (say, increase queue throughput or add a new analytics node), the change is made in code and applied across both domains, rather than tweaking one side and forgetting the other.

This unified approach reduces the operational fragmentation that plagues hybrid setups. GEICO’s team, for example, highlighted that when infrastructure spans multiple environments or vendors, operations can fragment into duplicated processes and inconsistent interfaces. IaC is a remedy for that fragmentation: it provides a single interface (the code) to manage different pieces of the hybrid estate.

Not only does IaC improve consistency, it also enhances visibility and control in a hybrid cloud. All infrastructure components, whether in Azure, AWS, or a private OpenStack cloud, are described in one place. This holistic view makes it easier to conduct impact analysis (e.g., see all systems dependent on a certain network segment) and apply global changes (like updating an OS version across all servers) reliably. It’s effectively an inventory and change management system for your hybrid cloud, built into your deployment process.

Finally, in terms of risk mitigation, hybrid cloud plus IaC is a powerful combination. Hybrid by nature mitigates some risk by not putting all eggs in one basket; IaC further mitigates risk by ensuring changes to that hybrid environment are done through tested, repeatable processes. This reduces the chance of misconfigurations that could cause outages or security exposures across the integrated environment. As one tech publication explained, defining every environment in code means you don’t worry about hidden config changes or diverging setups – if something goes wrong, you can rapidly roll back to a known good state.

For an insurer, that kind of resilience is gold. If a deployment to the hybrid cloud introduces an issue, the team can pinpoint the last code change and undo it, restoring the previous stable infrastructure in minutes.

In summary, hybrid cloud is here to stay in insurance, and IaC is what makes hybrid cloud operationally feasible at scale. Together they let insurers enjoy cloud benefits without abandoning reliable legacy systems overnight. The cloud journey doesn’t have to be an “either/or” choice; it can be a “both/and” – and with IaC, that combined estate can be managed with coherence, efficiency, and security.

From Lift-and-Shift to Cloud-Native Platforms

Not all cloud migrations are created equal. In the insurance industry’s early forays into cloud, a common approach was the “lift-and-shift” – essentially rehosting existing systems on cloud infrastructure with minimal changes. This strategy offers speed and lower immediate risk: legacy applications are moved out of aging data centers into modern cloud VMs largely as-is, gaining some infrastructure benefits (e.g. newer hardware, better network resilience) without requiring code overhaul.

Many insurers started their cloud journey this way, treating the cloud as just a different hosting environment for the same applications. The advantage was quick wins – reduced data center footprint, some OpEx cost conversion, and avoidance of large redevelopment efforts. However, lift-and-shift comes at a cost to long-term innovation. As experts note, this approach fails to fully capitalize on cloud’s potential.

The applications remain the same at heart, and insurers often find that simply running old COBOL or batch-based systems in the cloud yields limited agility or cost benefit. You might reduce some hardware maintenance expenses, but you won’t suddenly be able to iterate faster or integrate easily with modern services, because the app itself hasn’t changed.

Recognizing this, modern cloud migration strategies in insurance are taking a more transformative path. Rather than treating the cloud as just “someone else’s data center,” leading insurers are re-architecting core systems to be truly cloud-native or adopting entirely new cloud-based platforms. Several patterns are evident. Some organizations choose to refactor their applications – breaking monolithic systems into microservices, containerizing workloads with Kubernetes or similar, and rewriting parts of the code to leverage cloud scalability and managed services.

This is a technical heavy lift, but it can extend the life and capabilities of proprietary systems by fundamentally improving their architecture. Other insurers opt for replacement via SaaS platforms – for example, replacing a legacy policy administration or claims system with a modern cloud-native core platform provided by a vendor (many core insurance software vendors now offer SaaS versions of their systems). This “repurchase” approach offloads much of the technical heavy lifting to the vendor and allows the insurer to essentially skip a generation of technology, moving straight to an as-a-service model. In property & casualty insurance, for instance, cloud-based core platforms from various providers have rapidly become the norm for new system deployments; Gartner observes that such solutions are now “almost ubiquitous” for insurers modernizing in North America.

The contrast between these approaches is stark. A lift-and-shift cloud migration might achieve the immediate goal of exiting the data center, but it often does little to improve product speed-to-market, customer experience, or long-term cost structure. In contrast, a cloud-native core platform (whether built in-house or adopted from a vendor) can unleash new capabilities – from real-time data analytics and AI-driven underwriting, to seamless integrations with insurtech ecosystems – that were nearly impossible on the old tech stack. The end-state vision for many insurers is a future where the business runs on a flexible, unified cloud platform (or a set of interoperable platforms) that can continuously evolve as market needs change. Achieving that vision requires going beyond basic “lift and shift” migration and embracing true transformation of the technology core.

It’s worth noting that most large insurers will mix and match strategies across their application portfolio. They might lift-and-shift some ancillary systems that are not worth rearchitecting (for example, a niche internal tool can simply be moved to an Azure VM).

At the same time, they may fully reinvent other systems – say, transforming a claims workflow by adopting a new cloud-based claims platform, or decomposing a customer-facing portal into cloud-native microservices. The key is to apply the right approach for each component based on its strategic importance, complexity, and ROI of change.

In this evolution from lift-and-shift to cloud-native, DevOps and Infrastructure as Code become critical enablers. When you refactor to microservices or adopt new cloud platforms, you inherently increase the number of moving parts in your architecture. A monolithic application might become dozens of microservices, each with its own cloud resources.

Manually managing these is untenable – this is why cloud-native architectures almost mandate the use of automation and IaC. Insurers making this leap invest heavily in CI/CD pipelines and IaC scripts to manage deployment of these new cloud-native components. For example, if you containerize underwriting logic into microservices, you’ll likely use IaC to provision the Kubernetes clusters, define the container registries, set up monitoring, etc., as code.

Every new microservice might come with a Terraform module or Helm chart defining its infrastructure needs. The alternative (point-and-click setup for each service) does not scale and would introduce errors quickly. Thus, IaC is a foundational element of becoming a cloud-native enterprise – it’s the only way to achieve the speed and consistency that cloud-native development demands.

As the EM360Tech analyst succinctly put it, “infrastructure provisioning stops being a one-off event and becomes a predictable, versioned capability… manual processes are replaced with code, and human error is significantly reduced”. Cloud-native insurance IT organizations treat their infrastructure as a product that evolves alongside the applications, with full automation ensuring reliability even as changes occur daily.

Another area where IaC supports this journey is in SaaS platform integration and configuration. If an insurer adopts a new SaaS policy admin system, the surrounding cloud infrastructure (identity management, networking, data lakes for reporting, etc.) can be set up via code to interface cleanly with the SaaS. Also, many SaaS platforms provide IaC-like capabilities or APIs for configuration, which can be integrated into the insurer’s automation pipelines.

The result is that even SaaS adoption, which on the surface is more about configuration than building, benefits from an IaC mindset – treat the configuration as code, and you get repeatability and auditability for your customizations on that SaaS.

In summary, the insurance industry’s cloud journey is trending from initial “lift-and-shift” experiments towards full cloud-native modernization. It’s a challenging but necessary progression to truly realize cloud’s benefits. Insurers that embrace this trend are re-platforming core systems to be more modular, scalable, and digital-ready.

And critically, they are backing these efforts with the cultural and tooling shifts of DevOps and Infrastructure as Code. By doing so, they position themselves to deliver new capabilities faster and operate with the kind of agility that today’s digital markets demand. The cloud is not just a place to run servers – it’s a catalyst to reinvent how insurance IT operates, and those who leverage IaC and modern practices will be best equipped to harness that catalyst effectively.

Conclusion: Leading with Vision and Pragmatism

The journey to cloud for insurance enterprises is undeniably complex – but it is also undeniably transformative. Those organizations that navigate the risks and friction points effectively are positioning themselves for the next era of industry leadership. Cloud adoption done right is not just an IT upgrade; it is a strategic enabler of growth. As McKinsey observes, companies that boldly lead on cloud migration are outperforming peers and unlocking immense business value – on the order of $1 trillion in EBITDA impact globally. In insurance, this translates to the ability to launch products faster, scale effortlessly to meet customer surges, harness AI and data for better risk decisions, and create the kind of seamless digital experiences that today’s customers expect.

To realize this promise, insurance executives must marry vision with pragmatism. The vision is the end-state: a modern, cloud-powered insurer that can adapt in real-time to market changes, delight customers with digital services, and operate with vastly improved efficiency.

But pragmatism is the path: acknowledging that this revolution cannot happen overnight, and steering through the many challenges we’ve discussed – legacy risk, cost management, integration, hybrid complexity – with a steady hand. Cloud is not a panacea; it demands clear strategy and disciplined execution. Modernizing core systems, for example, requires meticulous risk management and likely a phased approach (with IaC ensuring each phase is stable).

Reaping cost benefits calls for ongoing optimization and sometimes tough choices about which workloads truly belong in the cloud. Integration challenges necessitate investing in modern architectures and talent. And embracing cloud’s full potential often means reimagining business processes on modern platforms, not merely lifting old ones over.

The encouraging news is that the industry’s collective experience is turning these challenges into a playbook for success. We are seeing insurers, even historically conservative ones, develop cloud migration muscles – learning from early missteps and steadily accelerating their adoption. Every hurdle cleared (be it technical, organizational, or regulatory) becomes a stepping stone toward a more agile, customer-centric, and competitive insurance business. Leaders are increasingly sharing best practices and success stories, which is helping the whole industry advance.

A key theme in those success stories is the empowerment of people and processes alongside technology. Cloud transformation isn’t just about new infrastructure; it’s about new ways of working. The insurers who are pulling ahead have often embraced DevOps and agile methods, broken down silos between IT and business, and instilled a culture of continuous improvement.

In this context, Infrastructure as Code has served as both a tool and a catalyst for cultural change – encouraging collaboration (developers and ops working off the same code base), transparency (everything documented in code), and rapid learning (fail fast, recover faster). Executives would be wise to champion these practices from the top. It sends a powerful message when a CIO or CTO emphasizes that infrastructure automation and DevSecOps are strategic priorities, not just engineering choices.

When cloud and DevOps leaders prioritize IaC and automation, they effectively future-proof the organization’s ability to adapt, because they are building a flexible foundation rather than hard-coding assumptions into manual configurations.

In the words of one technology leader, we are at a point where the right strategy can transform perceived roadblocks into pathways for innovation and growth. With a cloud-forward vision anchored in the realities of legacy environments, insurance organizations can indeed modernize without compromising stability. The winners in this cloud journey will be those who stay true to their strategic north star – leveraging cloud technology to create value, deepen resilience, and empower their people – while expertly steering through the practical challenges along the way. This means having the executive resolve to invest in modernization (even when it’s complex), the wisdom to use hybrid strategies and IaC as stabilizing forces, and the discipline to govern the new cloud era as tightly as the old.

By leading with both bold vision and pragmatic execution, insurers can turn cloud migration from a risky endeavor into a platform for reinvention. They are not just adopting new IT infrastructure, but building the digital insurance platforms of the future – platforms that will underpin the next generation of insurance products, services, and customer experiences. And Infrastructure as Code, alongside other modernization best practices, will ensure those platforms are robust, secure, and ready to drive growth in the years ahead.

In conclusion, cloud migration in insurance is a story of evolution with intention. It’s about harnessing cutting-edge technology (like IaC, AI, and cloud services) in a way that respects the complexity of the insurance business.

Those insurers that can do this – that can innovate quickly and manage risk diligently – are poised to define the future of the industry. The journey is challenging, yes, but the destination is one where insurers operate at the speed of tech companies, delight customers like never before, and achieve efficiencies that eluded their legacy-bound predecessors. With the right roadmap, tools, and mindset, the insurance industry’s cloud migration can indeed turn historic roadblocks into gateways to a brighter, more digital future.

Written by: Lior Herman, Co-Founder and CPO at ORBITInsure LLC | CEO & Founder Herman Technologies.

Cloud Adoption and Hybrid Cloud Statistics

Legacy IT Spend and Modernization Data

Cloud Migration Risk Estimates

GEICO Cloud Repatriation Case

Infrastructure as Code: Benefits and Practices

IaC as a Strategic Priority

IBM on IaC Eliminating Configuration Drift

Hybrid Cloud Advantages in Insurance

Primary Industry Insights

Herman Technologies, December 2025

(herman-technologies.com